By Anko Beldsnijder and Richard Burkhardt - avant garde capital

On the occasion of the inauguration of Ferrari's new E-Building in Maranello, we take a closer look at the shares of the Italian luxury sports car manufacturer in this edition of „Investments Explained“. Ferrari emerged from the racing division of Alfa Romeo in 1939. The first car produced in 1947 bore the surname of founder Enzo Ferrari. With its entry into Formula 1 in 1950 and winning the world championship for the first time in 1952, the Italian brand established itself as the world's leading racing car manufacturer.

With its spin-off from the Fiat Chrysler Automobile Group, Ferrari went public in 2015 and has been hot property among investors ever since. The Ferrari brand stands for passion, performance, design and exclusivity. To ensure the brand's attractiveness, the company ensures that demand always exceeds supply and that the order backlog is always greater than 12 months. Therefore, Ferrari shares cannot be compared with premium car manufacturers such as Mercedes or BMW, but rather with very exclusive luxury brands such as Hermès (where customers are also put on a long waiting list for handbags). The Italians continuously revise their product range and are also increasingly focusing on innovations in hybrid and electric technology. Hallmarks of this strategy include diversification (such as with the SUV Purosangre) or offering special editions in highly limited quantities. The life cycles of a car model are also shorter at 3-5 years than with traditional car manufacturers. This „scarcity strategy“ even means that not everyone who wants to drive such a car gains access to the exclusive club of Ferrari owners. Often, one must already own a sports car of the brand, have otherwise established relationships with a Ferrari dealer, or have been directly invited to purchase one. Those who are allowed to order a Ferrari can then customize it down to the last detail (which is also very profitable for the company itself). For these reasons, waiting times for a new car are often as long as two years, and it is considered a status symbol to even be on the waiting list.

To continue successfully advancing the strategy, the aforementioned E-Building was completed in June 2024. With the new plant, Ferrari could produce 20,000 instead of the previous 14,000 vehicles per year, but the brand continues to focus on quality rather than quantity. Therefore, the E-Building serves more to become more flexible in production and, above all, to manufacture the new hybrid and electric sports cars there, which now account for almost 50 percent of sales. In recent years, the company has been able to increase its revenue annually in the double-digit percentage range, which is unlikely to change in the future due to the expansion of the product portfolio.

Analysts expect average revenue growth of just under 10%. Thanks to the more flexible production in the new E-Building, the margin (Ebitda), which already stands at 27%, will also be able to increase by just under 100 basis points per year in the coming years. Net profit should therefore increase by approximately 11-12% per year. In addition, investors receive a dividend of just under 1% per year, and the company is buying back shares worth a total of 2 billion euros by 2026. Since debt has been reduced to a very low level (0.5x Net Debt/Ebitda) in recent years, there should be no obstacles to extending the share buyback program. A return on equity of almost 40% also confirms the high quality of the company.

![]()

Bereit für bessere Investment-Entscheidungen?

Starten Sie noch heute mit Ihrer kostenlosen Testphase - Aktienanalyse mit künstlicher Intelligenz.

Volle Transparenz | Voller Zugriff | Jederzeit kündbar

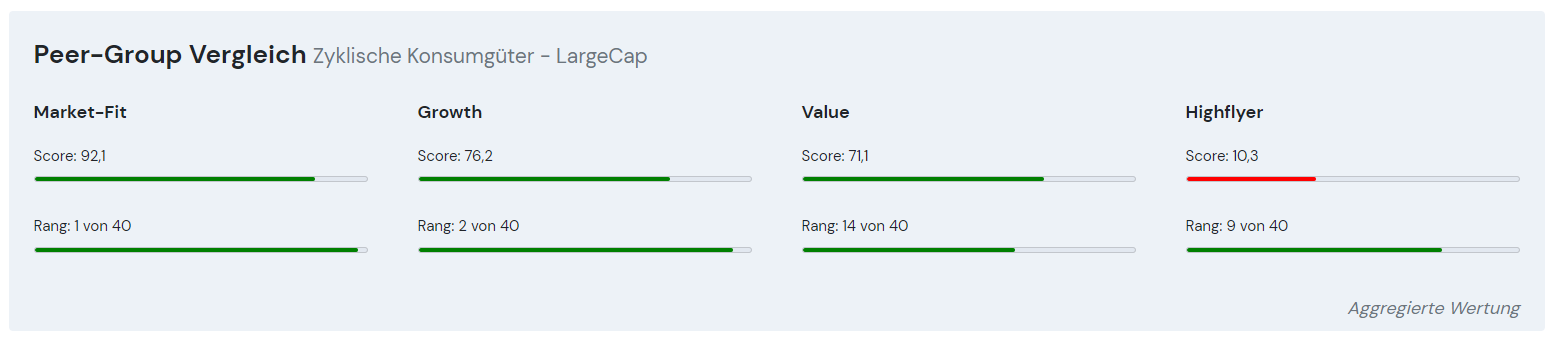

Since it is no longer a secret that Ferrari is a structurally high-growth company with very high visibility and the stock exhibits only moderate volatility, the valuation with a 2025 P/E of 44x and an EV/Ebitda of 25x is no longer a bargain. From a pure GARP perspective, the stock therefore appears (too) expensive. However, we invest using an AI-GARP approach, and Ferrari is therefore a good example of how pattern recognition with Artificial Intelligence (AI) from Leeway can create added value. The AI forms comparison groups by sector, market value and region and examines the influence of 18 factors from the areas of profitability, financial development and price-performance ratio on the performance of a stock compared to its peer group. As a result, the AI determines that in Ferrari's direct comparison group of sports car manufacturers, stocks with higher valuations also have a higher probability of further outperformance. Since the beginning of the year, when AI was consistently used in the portfolio construction process, Ferrari has achieved a return of 25%.

In Leeway's Market-Fit Rating, Ferrari achieves the best industry score with 92.1 out of 100 points and has consistently ranked in the top group of the consumer goods industry in recent years. The algorithm particularly positively evaluates the high return on equity and high margins. The company's financial risk is assessed as very low. For Leeway, the company's higher valuation is not a negative signal, but rather a confirmation that further outperformance is emerging.